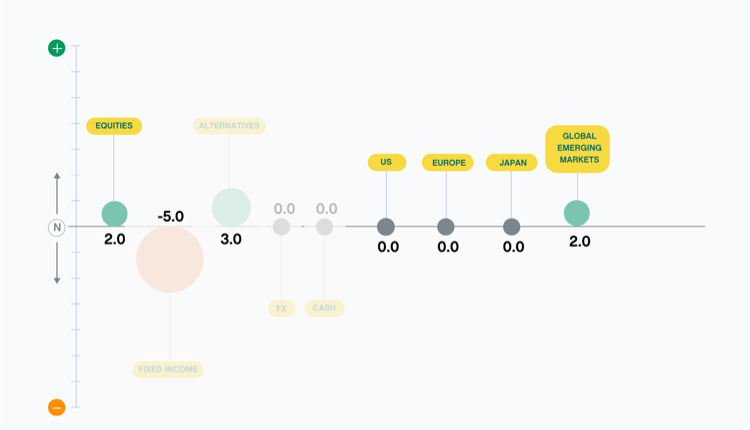

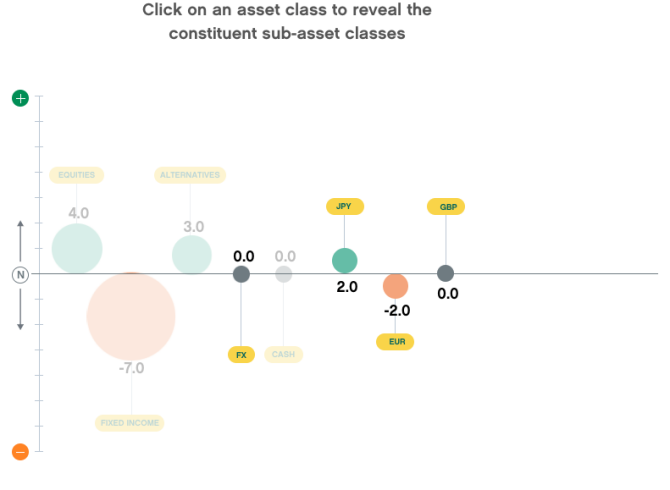

Click an asset class to show the sub-asset classes

The asset

allocation vector

"Over time the balance of risk should improve"

After immediate uncertainties resolve the economy can recover

THE PATH TO ESCAPE VELOCITY

Investment focus

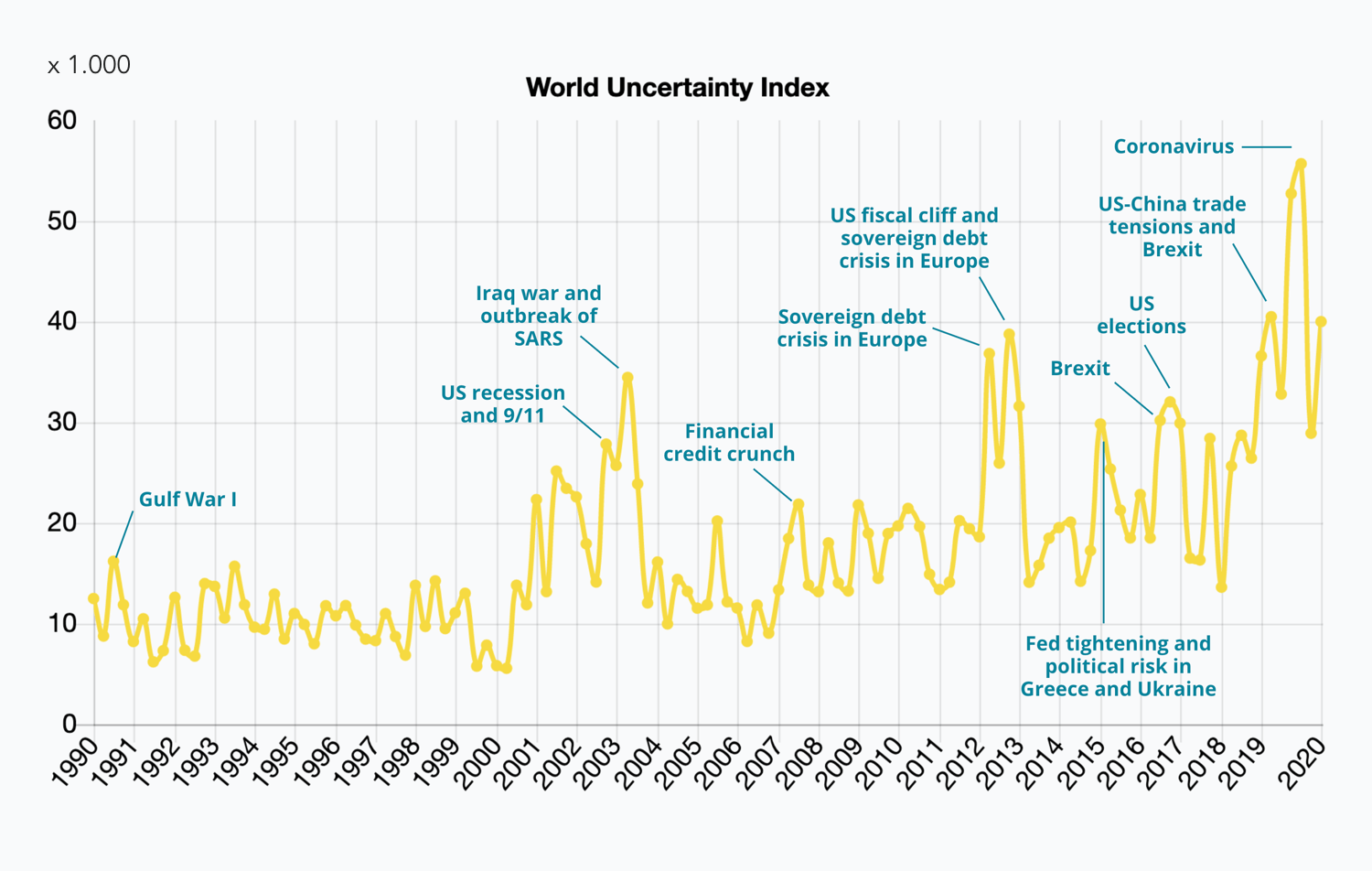

higher market volatility and slower economic growth. Although lower than during the worst days of the Covid-19 pandemic, uncertainty is on the rise again.

The World Uncertainty Index is based on the frequency that “uncertainty” appears in the media and country risk reports. Historically, increases have typically been associated with

The world is starting to feel more uncertain again

FEELING UNSETTLED

Top chart

The pandemic has forced us all to adapt and develop new skills

FASTER, HIGHER, STRONGER

Welcome

The pandemic has given us an opportunity to prove how quickly we can adapt. Working from home has its challenges, but what if you’d been training for an elite sporting event that was suddenly cancelled? We spoke to six Paralympians about how their lives changed as a result of the global health crisis. Read about their experiences here.

Members of my team, the Chief Investment Office, are located in Luxembourg, Belgium, Switzerland, Germany, the Netherlands, Spain and the UK. It has been a difficult year, but I’m proud of how we’ve worked together to adapt. The upcoming quarter presents challenges, but we see this as a speed bump – not a reason to despair. I hope you enjoy this month’s update.

Bill Street

Group Chief Investment Officer

Scroll down

Hitting a speed bump

COUNTERPOINT OCTOBER 2020

We’ve repositioned portfolios to reflect the risks in the market

UPDATE ALERT

Quintet portfolio

this we have closed our overweight in US equities.

In order to preserve the balance of risk across our full portfolio, we have also closed our overweight allocation to the Japanese yen, a position we held as a portfolio diversifier. The yen remains undervalued, but we don’t believe there are catalysts that could push up the currency closer to its fair value any time soon.

As long term investors with a positive outlook over the medium and long term, we maintain our ‘risk-on’ view. However, in order to reflect the immediate risks we have adjusted our tactical allocation.

The US, in particular, faces short term risks. The election is just over a month away and Covid-19 cases continue to rise. To address

Monitor

Portfolio

Investment focus

Top chart

Welcome

Monitor

Portfolio

Investment focus

Top chart

Welcome

Brexit

Iraq war and outbreak of SARS

Source: Ahir, H, N Bloom, and D Furceri (2018), “World Uncertainty Index”, Stanford mimeo

(Quintet estimates for Q3 based on daily data from www.policyuncertainty.com)

x 1.000

Gulf War I

US recession and 9/11

Financial credit crunch

Sovereign debt crisis in Europe

Fed tightening and political risk in Greece and Ukraine

US fiscal cliff and sovereign debt crisis in Europe

US elections

Coronavirus

US-China trade tensions and Brexit

We continue to believe the global economy will recover, with governments and central banks committed to supporting the healing process with stimulus measures and policies. Over time, the economy will reach escape velocity where the private sector will no longer rely on public support. Yet today significant uncertainties exist which will remain key challenges over the short term.

The rate of new infections has been rising in many regions, including parts of the US and Europe. Economic activity is likely to decelerate and could even contract in some regions as measures to slow the spread of Covid-19 are reintroduced. But governments hope to avoid full-scale lockdowns and, provided therapeutic progress continues, with ongoing support from governments, we expect that the pace of growth should pick up again early next year.

This document has been prepared by Quintet Private Bank (Europe) S.A. This document is defined as non-independent research because it has not been prepared in accordance with the legal requirements designed to promote the independence of investment research, including any prohibition on dealing ahead of the dissemination of this information.

This document is of a general nature and does not constitute legal, accounting or tax advice. This document does not provide any individual investment advice and an investment decision must not be based merely on the information and data contained in the document.

All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

The statements and views expressed in this document based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 28 September, 2020 and are subject to change.

Invest in a richer life,

however you define it.

Thank you for reading our monthly update. Please contact us if you have any questions, remarks or suggestions regarding this update.

WE TAKE TIME TO LISTEN

Counterpoint October 2020

TRADE US–China trade tensions

TRADE UK–EU trade negotiations (Oct/Dec)

POLITICAL US Presidential election (Nov)

MEDICAL Search for vaccine

FISCAL EU Recovery Fund (Q3/Q4)

FISCAL Next US fiscal package (Q3 / H1 2021)

MONETARY Global central banks

Outlook is more certain than last month

Outlook is less certain than last month

As we move into the fourth quarter uncertainty has increased

WHAT TO LOOK

OUT FOR

Monitor

Back to top

Copyright © Quintet Private Bank (Europe) S.A. 2020. All rights reserved. Privacy Statement

As long term investors with a positive outlook over the medium and long term, we maintain our ‘risk-on’ view. However, in order to reflect the immediate risks we have adjusted our tactical allocation.

The US, in particular, faces short term risks. The election is just over a month away and Covid-19 cases continue to rise. To address this we have closed our overweight in US equities.

In order to preserve the balance of risk across our full portfolio, we have also closed our overweight allocation to the Japanese yen, a position we held as a portfolio diversifier. The yen remains undervalued, but we don’t believe there are catalysts that could push up the currency closer to its fair value any time soon.

This document has been prepared by Quintet Private Bank (Europe) S.A. This document is defined as non-independent research because it has not been prepared in accordance with the legal requirements designed to promote the independence of investment research, including any prohibition on dealing ahead of the dissemination of this information.

This document is of a general nature and does not constitute legal, accounting or tax advice. This document does not provide any individual investment advice and an investment decision must not be based merely on the information and data contained in the document.

All investors should keep in mind that past performance is no indication of future performance, and that the value of investments may go up or down. Changes in exchange rates may also cause the value of underlying investments to go up or down.

The statements and views expressed in this document based upon information from sources believed to be reliable – are those of Quintet Private Bank (Europe) S.A. as of 28 September, 2020 and are subject to change.

Invest in a richer life,

however you define it.

Copyright © Quintet Private Bank (Europe) S.A. 2020. All rights reserved. Privacy Statement

Back to top

POLITICAL

US Presidential election

(Nov)

MEDICAL

Search for vaccine

FISCAL

EU Recovery Fund

(Q3/Q4)

FISCAL

Next US fiscal package

(Q3 / H1 2021)

MONETARY

Global central banks

We’re also heading into a period where there’s a lot of political uncertainty. Although Joe Biden is ahead in the US presidential election polls, recent history reminds us that the unexpected is not impossible. Meanwhile, the UK is scheduled to leave the European Union on 31 December.

We believe the recovery should gain momentum in early 2021 provided therapeutics get better and lockdowns relax once again. Regardless of who wins the US elections, the Democrats and Republicans should have breathing space to agree a new rescue package. Meanwhile, although Brexit is an extra source of uncertainty for the time being, both sides will at last be able to move on with their new lives once the process is resolved.

Over time the balance of risk should improve. Ultimately, underlying structural forces on the economy, such as the transition from physical to digital, are expected to continue to change the economy and drive growth over the longer term.

Welcome

"Over time the balance of risk should improve"

We continue to believe the global economy will recover, with governments and central banks committed to supporting the healing process with stimulus measures and policies. Over time, the economy will reach escape velocity where the private sector will no longer rely on public support. Yet today significant uncertainties exist which will remain key challenges over the short term.

The rate of new infections has been rising in many regions, including parts of the US and Europe. Economic activity is likely to decelerate and could even contract in some regions as measures to slow the spread of Covid-19 are reintroduced. But governments hope to avoid full-scale lockdowns and, provided therapeutic progress continues, with ongoing support from governments, we expect that the pace of growth should pick up again early next year.

The World Uncertainty Index is based on the frequency that “uncertainty” appears in the media and country risk reports. Historically, increases have typically been associated with higher market volatility and slower economic growth. Although lower than during the worst days of the Covid-19 pandemic, uncertainty is on the rise again.

The pandemic has given us an opportunity to prove how quickly we can adapt. Working from home has its challenges, but what if you’d been training for an elite sporting event that was suddenly cancelled? We spoke to six Paralympians about how their lives changed as a result of the global health crisis. Read about their experiences here.

Members of my team, the Chief Investment Office, are located in Luxembourg, Belgium, Switzerland, Germany, the Netherlands, Spain and the UK. It has been a difficult year, but I’m proud of how we’ve worked together to adapt. The upcoming quarter presents challenges, but we see this as a speed bump – not a reason to despair. I hope you enjoy this month’s update.

Hitting a speed bump

COUNTERPOINT OCTOBER 2020

TRADE

US–China trade tensions

TRADE

UK–EU trade negotiations

(Oct/Dec)

Top chart

The world is starting to feel more uncertain again

FEELING UNSETTLED

Top chart

The asset allocation vector

Click an asset class to show the sub-asset classes

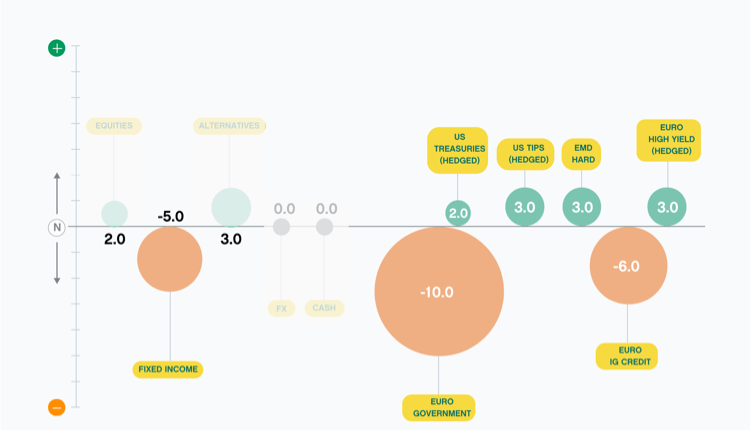

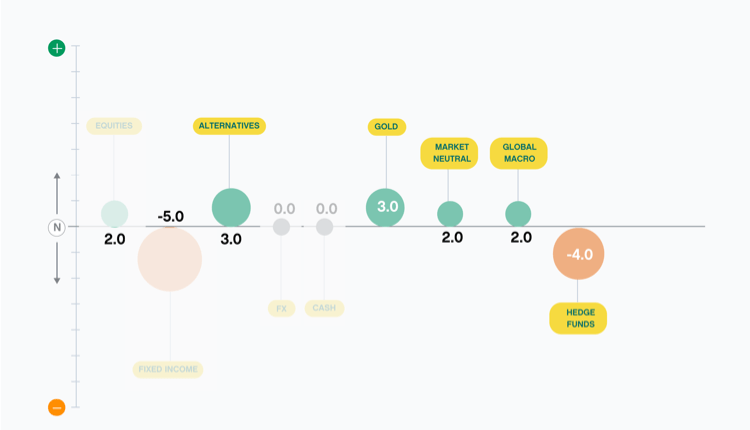

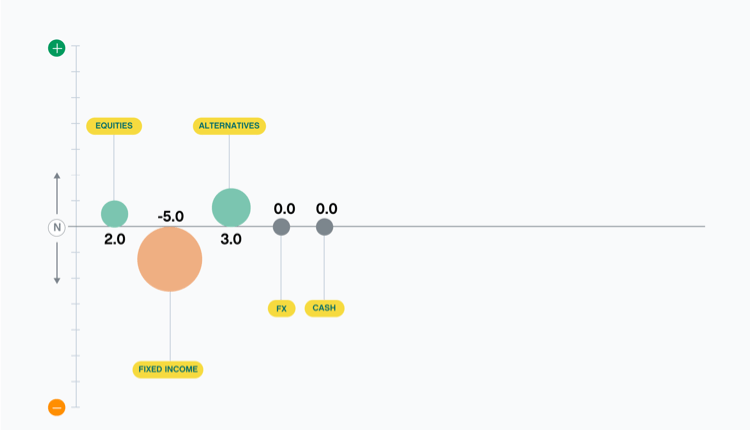

The view of each asset class is made up of sub-asset class views. Although we are negative on fixed income overall (-5%) there are areas where we see potential, such as Euro High Yield (+3%). The sum of the sub-asset class adjustments for each asset class represents the total asset class adjustment.

The specific numerical weights given here relate to a EUR balanced portfolio and can be adjusted for different profiles.

How to interpret the vector

A positive view means that we see more value in an asset class or sub-asset class and hold more than the benchmark allocation (overweight). A negative view means we hold less than the benchmark allocation (underweight). The sum of the weights across all asset classes is zero – if you increase in one area you need to decrease in another. Overall, relative to our EUR balanced benchmark we currently hold 5% less of the portfolio in fixed income and instead hold 2% more in equities and 3% more in alternatives.

Our asset allocation vector explained

Thank you for reading our monthly update. Please contact us if you have any questions, remarks or suggestions regarding this update.

WE TAKE TIME TO LISTEN

Counterpoint October 2020

Outlook is less certain than last month

Outlook is more certain than last month

As we move into the fourth quarter uncertainty has increased

WHAT TO LOOK

OUT FOR

Monitor

We’ve repositioned portfolios to reflect the risks in the market

UPDATE ALERT

Quintet portfolio

After immediate uncertainties resolve the economy can recover

THE PATH TO ESCAPE VELOCITY

Investment focus

Swipe to see the full graph

Source: Ahir, H, N Bloom, and D Furceri (2018), “World Uncertainty Index”, Stanford mimeo

(Quintet estimates for Q3 based on daily data from www.policyuncertainty.com)

Bill Street

Group Chief Investment Officer

Investment focus

The pandemic has forced us all to adapt and develop new skills

FASTER, HIGHER, STRONGER

Welcome

Monitor

Portfolio